AEC Sector Gains Hope with Federal Reserve's Interest Rate Cut: Archinect’s August 2024 Overview

Welcome to the latest edition of Archinect’s State of AEC, where we delve into the economic pulse of the architecture and construction industries. As we step into September 2024, there's a renewed sense of optimism following the Federal Reserve's decision to lower interest rates. This move has sparked hopes for a revitalized growth trajectory in both design studios and construction sites.

In our previous update, we highlighted the industry’s collective anticipation for a rate cut. Well, those hopes have been realized. The Federal Reserve has confirmed that starting in September, interest rates will see a reduction. While the long-term impact remains to be seen, we’re already observing varied trends across the architecture and construction sectors.

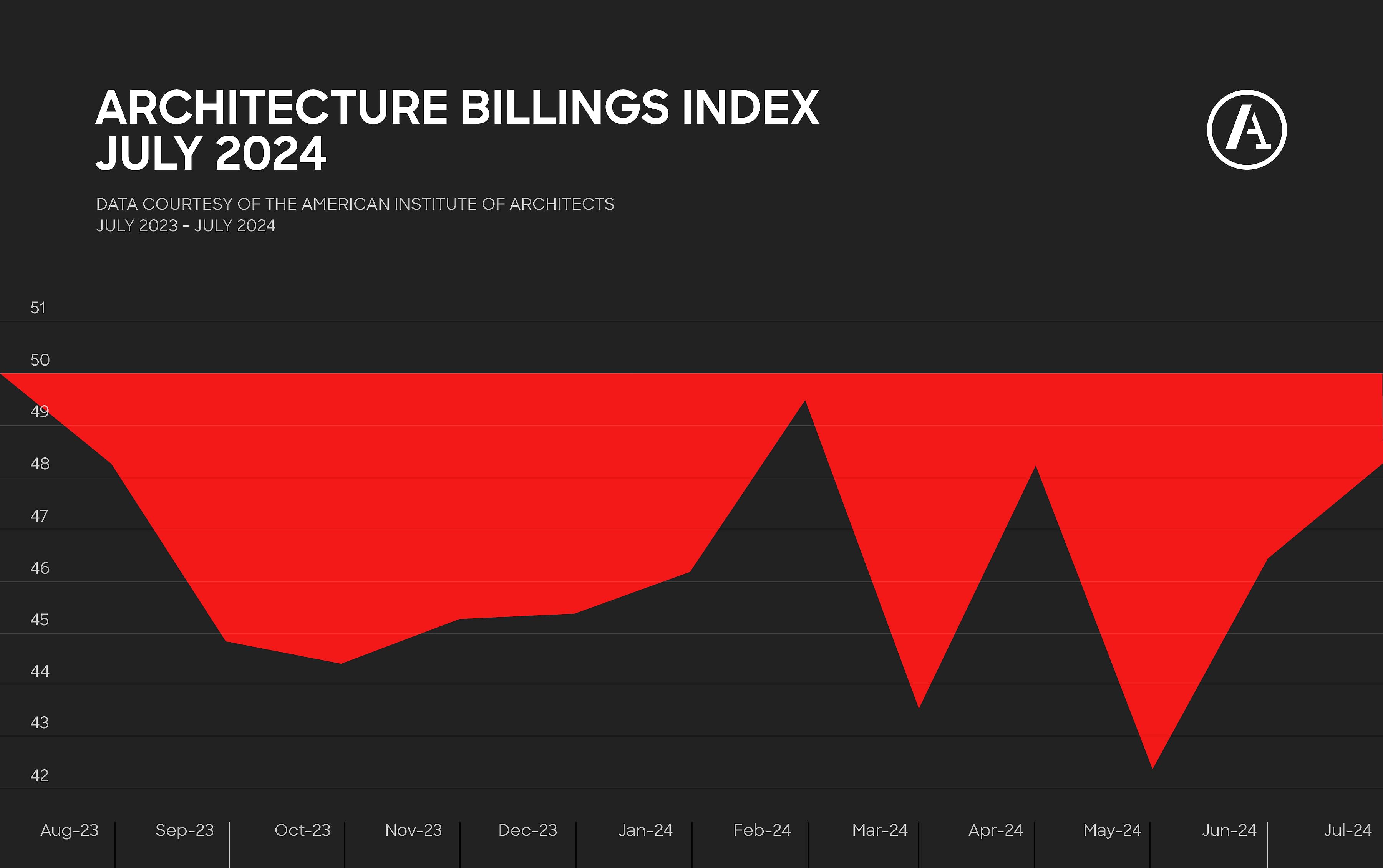

Let’s start with the architecture side. The American Institute of Architects (AIA) Architecture Billings Index (ABI) for July 2024 reveals a continued decline in billings, albeit at a slower pace than previous months. The ABI score of 48.2 suggests that more firms reported a drop in billings than an increase. However, it’s worth noting that there has been a steady rise in new inquiries over the past year, though the dollar value of new contracts has been decreasing. The AIA predicts slower growth in the next six months due to uncertainties surrounding the upcoming election, domestic policies, and global tensions.

Also Read:- Indiana Fever’s Return to the Playoffs: A Season of Resurgence

- Small Asteroid to Burn Up Over Philippines in Spectacular Display

Regional variations are also notable. In the Northeast, architecture firms experienced stable business conditions with no significant change in billings, while construction starts increased. The Midwest saw a slight improvement in business conditions, although billings remained in decline. The West, which has been struggling with prolonged billing declines, saw some improvement in construction starts, but still faces a 22-month streak of downturns. The South continues to face a deteriorating trend in business conditions, although the rate of decline has lessened.

Turning to the construction sector, there’s a brighter picture. Total construction starts in the U.S. rose by 10% last month, a promising sign after a period of volatility. This uptick is driven by significant increases in nonresidential and infrastructure projects. The Dodge Momentum Index, which tracks the value of nonresidential projects in planning, saw a notable 7.9% increase, suggesting a resurgence in planning activity across various sectors.

Despite this positive momentum, there are challenges. Construction material costs have risen slightly, though this is tempered by a decrease in softwood lumber prices. The Associated Builders and Contractors’ Construction Confidence Index indicates that while contractors remain cautiously optimistic, they anticipate only marginal improvements in profit margins over the next six months.

Regionally, the construction landscape shows mixed signals. The Northeast and Midwest have seen increases in total construction starts, while the West and South have experienced modest gains. The residential sector, particularly multifamily construction, remains strong, hitting a 50-year high, although single-family starts have declined.

In summary, the Federal Reserve’s interest rate cut has injected a dose of optimism into the AEC sector. As we move forward, the industry will be watching closely to see how these economic shifts impact project planning, construction activity, and overall business health. For a deeper dive into the nuances of these trends, check out our comprehensive survey results and analysis of the current economic conditions in the architecture profession.

Stay tuned to Archinect for ongoing updates and insights into the evolving state of AEC.

Read More:

0 Comments